Table Of Content

Currently, the Federal Reserve is actively buying 10-year Treasury notes, which increases the demand for these securities and drives their price up and yields down. So, our near record low mortgage rates are directly tied to the Federal Reserve Board's response to COVID-19 in efforts to keep financial markets open. When it begins to taper (stop purchasing 10-year Treasury notes) significantly, mortgage rates will rise.

Down payment

CNET staff -- not advertisers, partners or business interests -- determine how we review the products and services we cover. Today, the mortgage interest rate on a 30-year fixed mortgage is 7.62%, according to Curinos, while the average rate on a 15-year mortgage is 6.86%. On a 30-year jumbo mortgage, the average rate is 7.63%.Current Mortgage Rates for April 25,... Today, the mortgage interest rate on a 30-year fixed mortgage is 7.68%, according to Curinos.

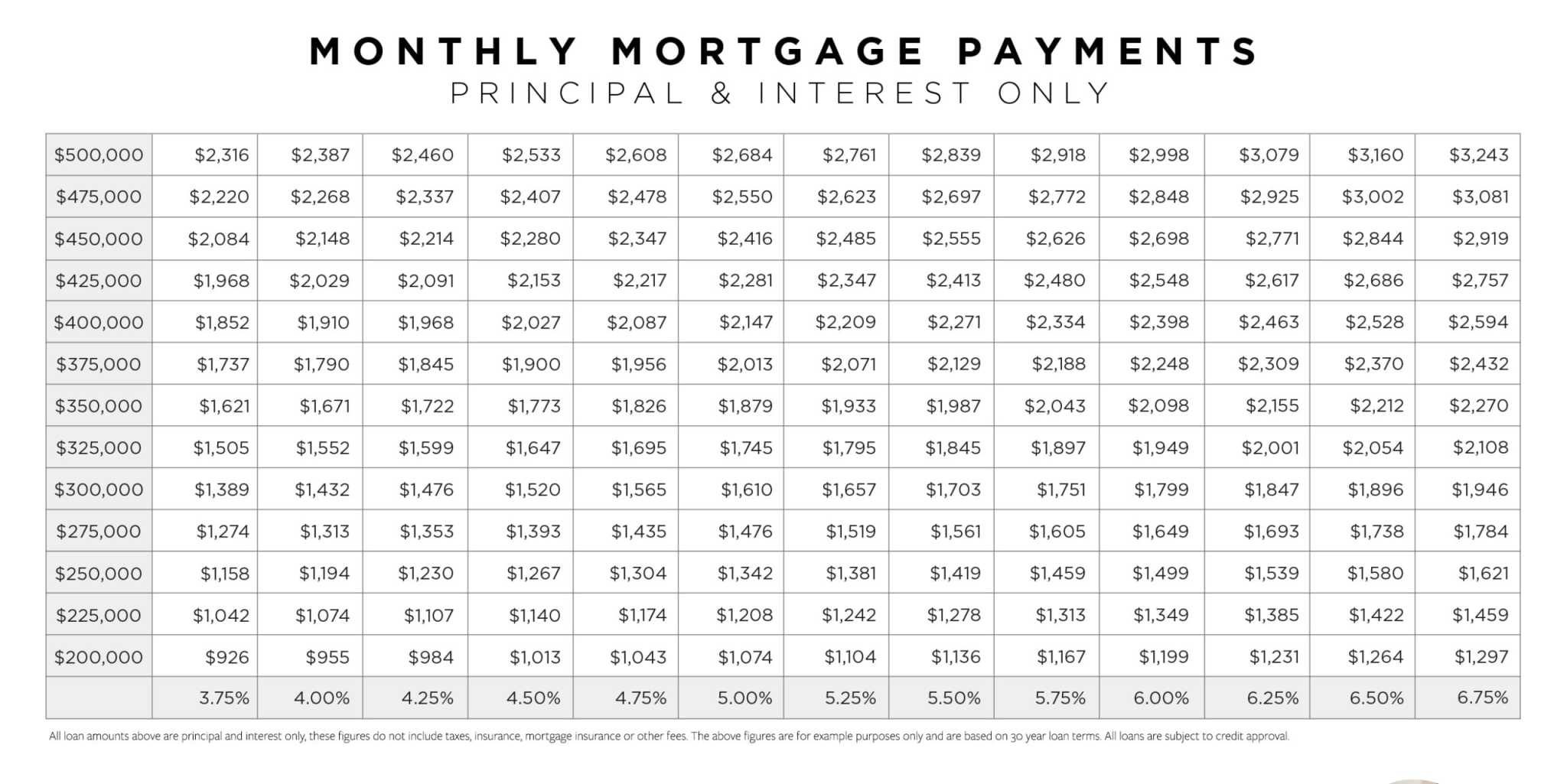

A look at mortgage rates over time

Mortgage Interest Rates Today, April 28, 2024 Rates Tick Up Following Inflation Report - Business Insider

Mortgage Interest Rates Today, April 28, 2024 Rates Tick Up Following Inflation Report.

Posted: Sun, 28 Apr 2024 10:00:00 GMT [source]

It’s possible to get the seller or lender to pay a portion or all of these costs. The current national mortgage rates forecast indicates that rates are likely to remain high compared to recent years, but could trend closer to 6% if inflation continues to decrease in 2024. This week, 30-year mortgage rates went up by 0.07% and 15-year rates increased by 0.05%.

Jumbo loans

Although fixed mortgage rates are not controlled by the Fed, their actions have undeniably contributed to a significant upward push in these rates. Locks are usually in place for at least a month to give the lender enough time to process the loan. If the lender doesn’t process the loan before the rate lock expires, you’ll need to negotiate a lock extension or accept the current market rate at the time. When you receive a mortgage loan offer, a lender will usually ask if you want to lock in the rate for a period of time or float the rate. If you lock it in, the rate should be preserved as long as your loan closes before the lock expires. But these predictions are based on assumptions that may or may not pan out.

Just remember, certain fees like homeowners insurance or taxes might not be included in the calculations. A complex set of factors impact mortgage interest rates, including broader economic conditions, the monetary actions of the Federal Reserve (to some extent) and inflation. However, long-term mortgage rates are directly impacted by the bond market. The rate you’re offered on a mortgage will also depend on the lender you work with, its business costs and your financial profile. If you want to pay off a 30-year fixed-rate mortgage faster or lower your interest rate, you may consider refinancing to a shorter term loan or a new 30-year mortgage with a lower rate. The best time to refinance will vary based on your circumstances.

Fox says his models suggest that rates will hover at 7.5% or higher throughout 2024. The good news is that, despite elevated rates, there are methods you can employ to secure a lower rate. These methods might be especially beneficial if you bought a home between mid-October and early November 2022 or mid-August through early December 2023 when rates were over 7%. Even so, Cohn expects the Fed to start cutting rates in June or July. Five years ago, the average rate was 4.2%, according to the Federal Reserve of St. Louis.

Current Home Equity Loan Rates - Buy Side from WSJ - The Wall Street Journal

Current Home Equity Loan Rates - Buy Side from WSJ.

Posted: Thu, 25 Apr 2024 16:08:00 GMT [source]

Conventional loans are backed by private lenders, like a bank, rather than the federal government and often have strict requirements around credit score and debt-to-income ratios. If you have excellent credit with a 20% down payment, a conventional loan may be a great option, as it usually offers lower interest rates without private mortgage insurance (PMI). You can still obtain a conventional loan with less than a 20% down payment, but PMI will be required.

With Federal Reserve voting to hold the federal funds rate steady in January and inflation heading closer to target, three rate cuts appear to be on the menu in 2024. This would be the first cut since the Fed slashed rates in the early days of the Covid-19 pandemic, although most experts don’t expect to see it happening until some point in the spring. With inflation running ultra-hot, mortgage interest rates surged to their highest levels since 2002. According to Freddie Mac’s records, the average 30-year rate jumped from 3.22% in January to a high of 7.08% at the end of October. The most important task for a prospective homeowner seeking a preapproval letter is to gather all the financial paperwork needed to give the lender a solid picture of your income, debts and credit history.

Weekly national mortgage interest rate trends

Several factors impact mortgage rates, including the repayment term, loan type and borrower’s credit score. The standard 30-year fixed rate mortgage is benchmarked off the 10-year U.S. The spread reflects the "cost" of the mortgage to an investor based on the risks that the borrower could prepay their loan down the road or default on the loan in the future. These costs rise and fall with general economic conditions, including the prevailing interest rate environment causing rates to rise and fall according to changes in the risk of these loans to investors. Market demand and supply forces are drivers of mortgage rates, as well.

The most important thing is to make a budget and try to stay within your means. CNET’s mortgage calculator below can help homebuyers prepare for monthly mortgage payments. Over the last few years, high inflation and the Federal Reserve’s aggressive interest rate hikes pushed up mortgage rates from their record lows around the pandemic.

Our scoring formula weighs several factors consumers should consider when choosing financial products and services. This table does not include all companies or all available products. The lower your rate, the more you'll be able to borrow, so shop around and get preapproved with multiple mortgage lenders to see who can offer you the best rate.

Some charge higher rates on jumbo loans, some charge lower rates for jumbo loans. Money can't buy happiness, but it can usually buy a lower mortgage interest rate. You pay a fee when you get the loan, and your lender permanently reduces your interest rate. Buying points could be a good strategy if you plan to own the home for a long time.

If conditions are choppy, and interest rates are likely to rise, it may be smart to lock in a rate that works with your budget and seems fair to you. Homebuilders have been able to mitigate the impact of elevated home loan borrowing costs this year by offering incentives, such as covering the cost to lower the mortgage rate home buyers take on. That’s helped spur sales of newly built single-family homes, which jumped 8.8% in March from a year earlier, according to the Commerce Department. The rise in mortgage rates in recent weeks is an unwelcome trend for home shoppers this spring homebuying season.

No comments:

Post a Comment